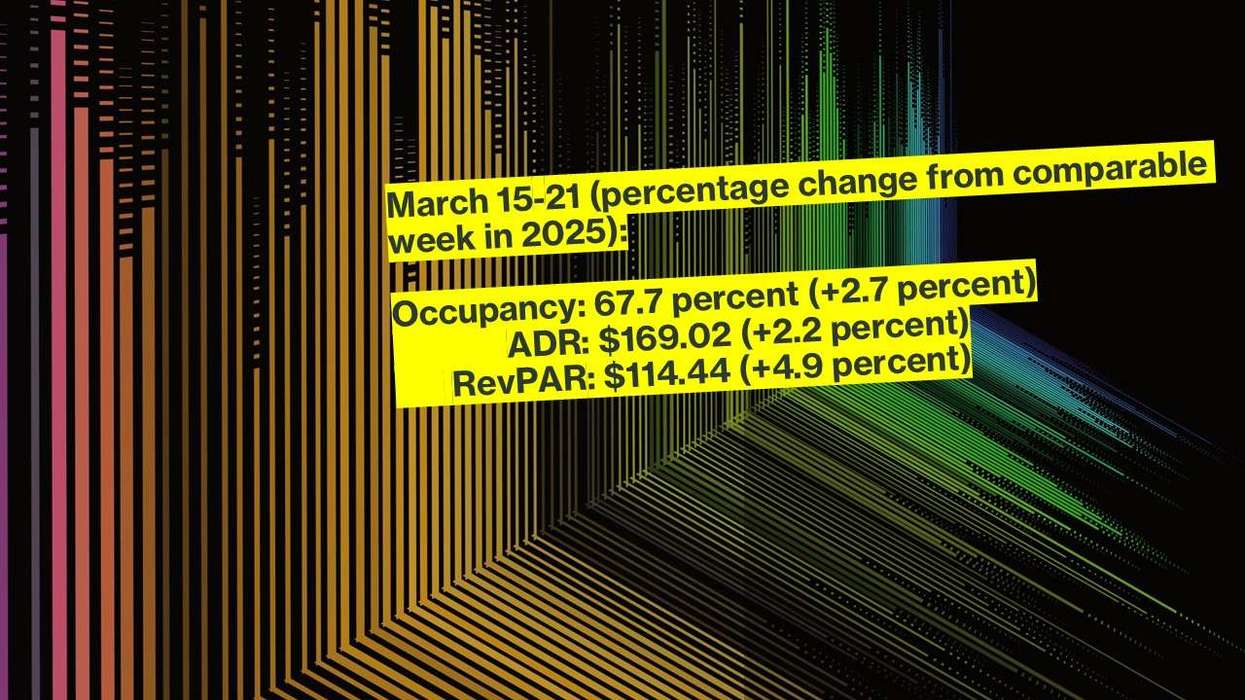

Photo credit: Cloudbeds Hospitality Market Data & Reports Report: OTAs top direct bookings for independents Vishnu Rageev R.Mar 29, 2026